Modular Space Holdings Files Chp 11 with a Pre-Pack

Today Modular Space Holdings and its affiliated debtors filed a petition for relief under Chp. 11 of the Bankruptcy Code in the District of Delaware while a wholly owned subsidiary, ModSpace Financial Services Canada (MFSC) commenced its proceedings under the CCAA in Toronto, respectively.

According to the first day declaration, "ModSpace is the largest U.S.-owned provider of temporary and permanent modular buildings, and is among the largest suppliers in the U.S. and Canada of temporary modular space and permanent modular construction."

According to the first day declaration, "ModSpace is the largest U.S.-owned provider of temporary and permanent modular buildings, and is among the largest suppliers in the U.S. and Canada of temporary modular space and permanent modular construction."

ModSpace occupies 142 locations including branch and service centers throughout N.A. with 639 employees. 41 locations are owned and 101 leased.

ModSpace's Corporate Structure is shown below:

Modspace's Capital Structure consists of $984.2m of outstanding long term debt and $37.7 of accrued interest.

$609.2 million of it is under an ABL facility, including $3.2 million of funded letters of credit, plus

accrued interest of $2.3 million as of today. $549.1 million on account of U.S. Borrowers and $60.1 million on

account of its Canadian Borrower. They have first priority on substantially of all the assets of the ModSpace.

$375 million of it is 10.25% Senior Secured Second Lien

Notes due 2019, plus outstanding and accrued interest of approximately $35.4 million as

of today.

With their business depending heavily on energy industries, the downtown in oil and other commodities has took a hit on their utilization rates and caused the Debtors to have problems with the maturity of their ABL in June 2016. In discussions with the ABL lenders they agreed to pursue a merger transaction with Williams Scotsman International which would provide significant synergies between the two companies. They were going to raise capital for the merger transaction by issuing equity, however the Brexit vote changed the minds of certain parties who, as a result backed out.

After discussions with additional financial advisors, and an Ad Hoc Group of Secured Noteholders, it was eventually decided not to proceed with the merger transaction, and both parties terminated the Merger Agreement. Thereafter, ModSpace would focus on a stand alone restructuring and in doing so engaged Lazard and Zolfo Cooper for assistance.

All parties finally were able to come to a Restructuring Support Agreement where the terms are as follows:

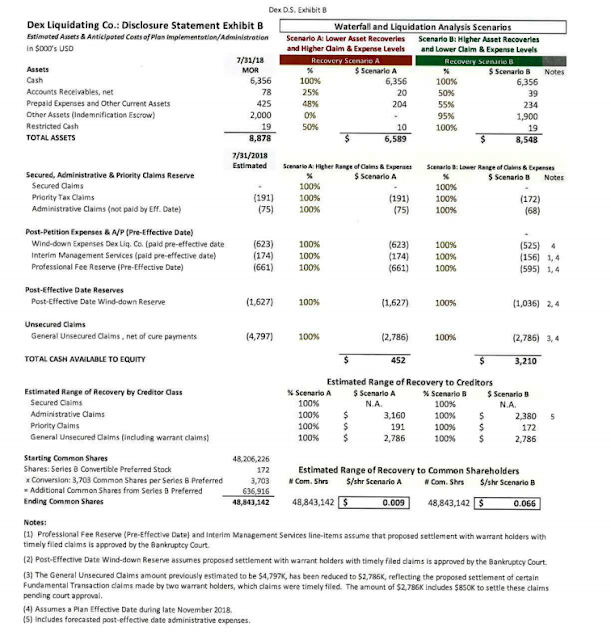

The POR valuation analysis done by Lazard provides the resulting company post emergence an enterprise value between $896 million and $1,107m (with a midpoint of $1,002m) and anticipates net debt of $553m, after taking into account the Rights Offering. This results in the equity being valued between $343m and $554m (with a midpoint of $449m)

Below are the projected financial statements:

All parties finally were able to come to a Restructuring Support Agreement where the terms are as follows:

The POR valuation analysis done by Lazard provides the resulting company post emergence an enterprise value between $896 million and $1,107m (with a midpoint of $1,002m) and anticipates net debt of $553m, after taking into account the Rights Offering. This results in the equity being valued between $343m and $554m (with a midpoint of $449m)

Below are the projected financial statements: